The Illusion of Wealth (Part IV)

Warren Buffett Returns, Berkshire Hathaway Performance & IPO Winners

This is Part IV of the "Illusion of Wealth" series tracking 100 years of dollar value dilution.

Table of Contents

If the only way to beat money printing was to compound above 6.56%, what was the best way to actually do it before the digital age?

Executive Summary

In Part III, we established the fundamental mathematical law of 20th-century wealth creation: The 6.56% Rule. Any asset compounding above the average monetary expansion rate of 6.56% beat the printing press. Anything below it lost.

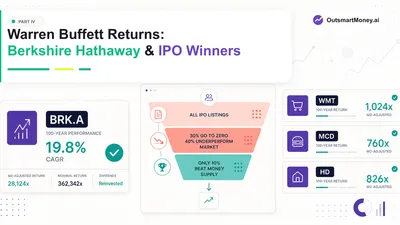

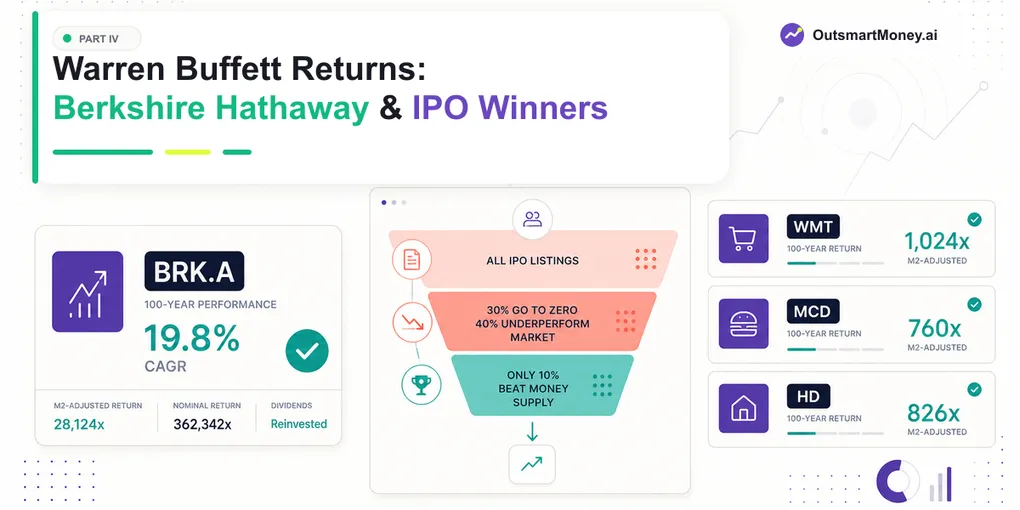

We also saw that Berkshire Hathaway, under Warren Buffett’s management, proved this rule emphatically by compounding at 19.8% over 60 years.

But was Berkshire Hathaway the only way to win? Or could an investor have simply picked the right “old economy” stocks at their Initial Public Offerings (IPOs) and achieved the same result?

This fourth part examines the generational non-tech IPO winners, from McDonald’s and Walmart to Home Depot and Nike, and compares them against both the money supply and Berkshire Hathaway. The data reveals that whilst picking the right IPOs yielded astronomical returns, the survivorship bias makes it an almost impossible strategy to execute in reality.

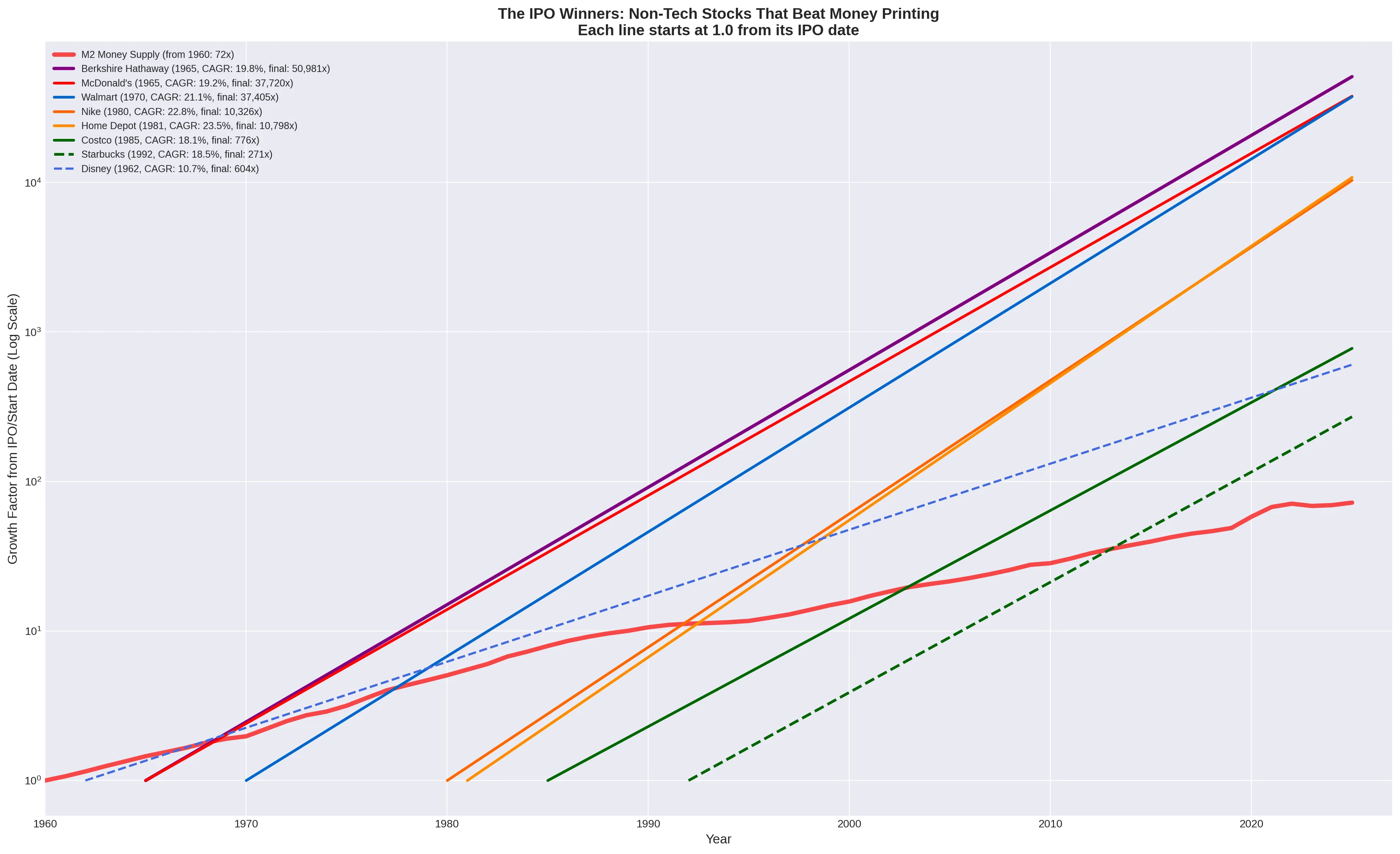

The Non-Tech IPO Winners: Beating the Printing Press

If you possessed a crystal ball in the second half of the 20th century, you did not need to invest in Berkshire Hathaway to build generational wealth. You simply needed to identify the consumer brands that would eventually dominate the American market, and hold them for decades.

The chart below plots the growth of these generational winners from their respective IPO dates, with each starting at a baseline of 1.0.

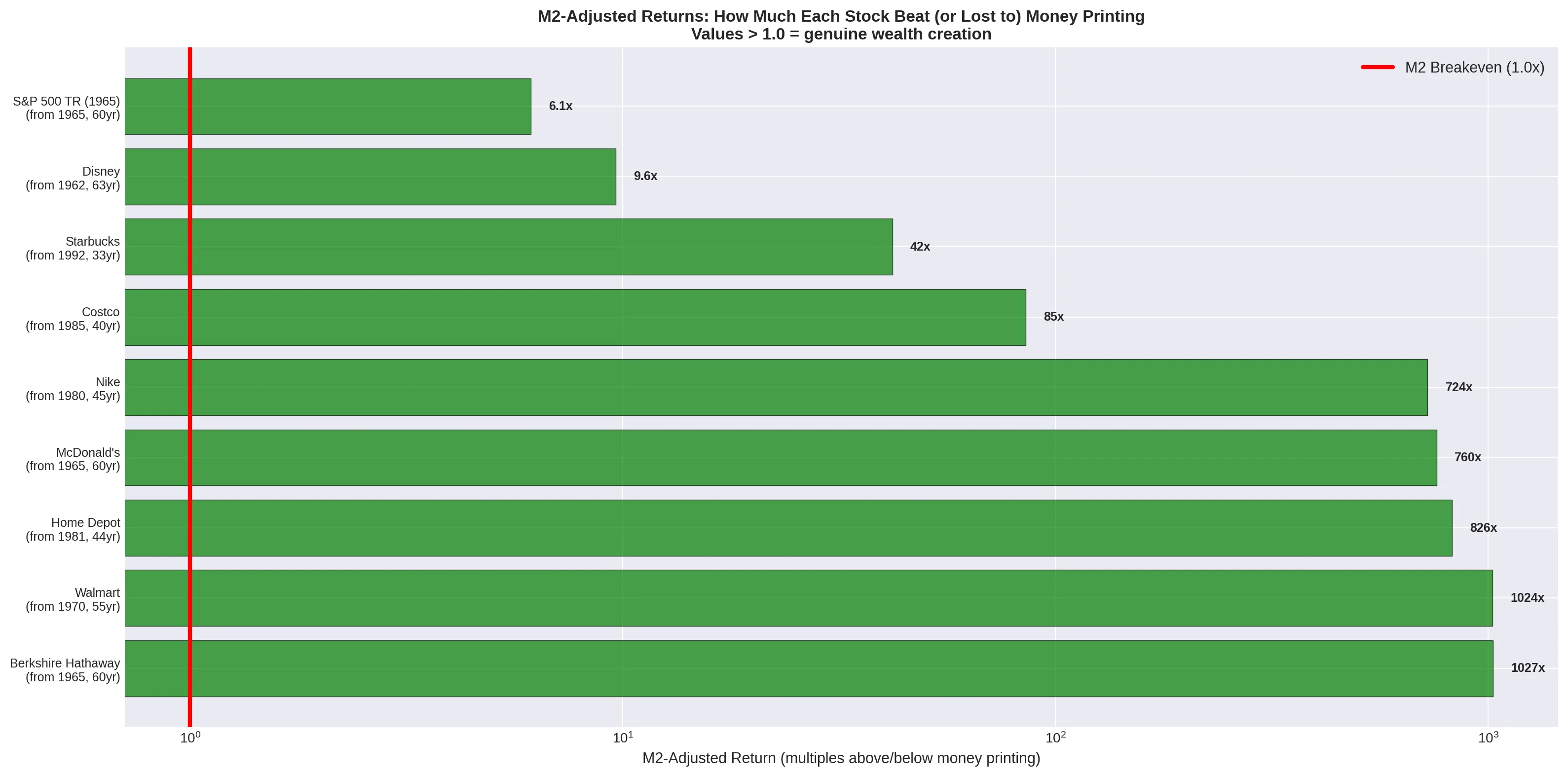

When we adjust these returns for the expansion of the M2 money supply over their respective holding periods, the results are striking:

| Stock | Start Year | Years Held | Nominal Growth | M2 Growth | M2-Adjusted Return | CAGR |

|---|---|---|---|---|---|---|

| Berkshire Hathaway | 1965 | 60 | 50,981x | 50x | 1,027x | 19.8% |

| Walmart | 1970 | 55 | 37,405x | 37x | 1,024x | 21.1% |

| Home Depot | 1981 | 44 | 10,798x | 13x | 826x | 23.5% |

| McDonald’s | 1965 | 60 | 37,720x | 50x | 760x | 19.2% |

| Nike | 1980 | 45 | 10,326x | 14x | 724x | 22.8% |

| Costco | 1985 | 40 | 776x | 9x | 85x | 18.1% |

| Starbucks | 1992 | 33 | 271x | 6x | 42x | 18.5% |

| S&P 500 Total Return | 1965 | 60 | 304x | 50x | 6.1x | 10.0% |

Data sourced from historical split-adjusted pricing [1] [2] [3]. M2 adjusted values indicate how many times the asset outpaced the money supply.

The data shows that Walmart and Berkshire Hathaway are in a dead heat for the title of the greatest wealth creator of the pre-digital era. Both effectively multiplied an investor’s true purchasing power by over 1,000 times, even after accounting for the massive expansion of the money supply.

The Survivorship Bias Problem

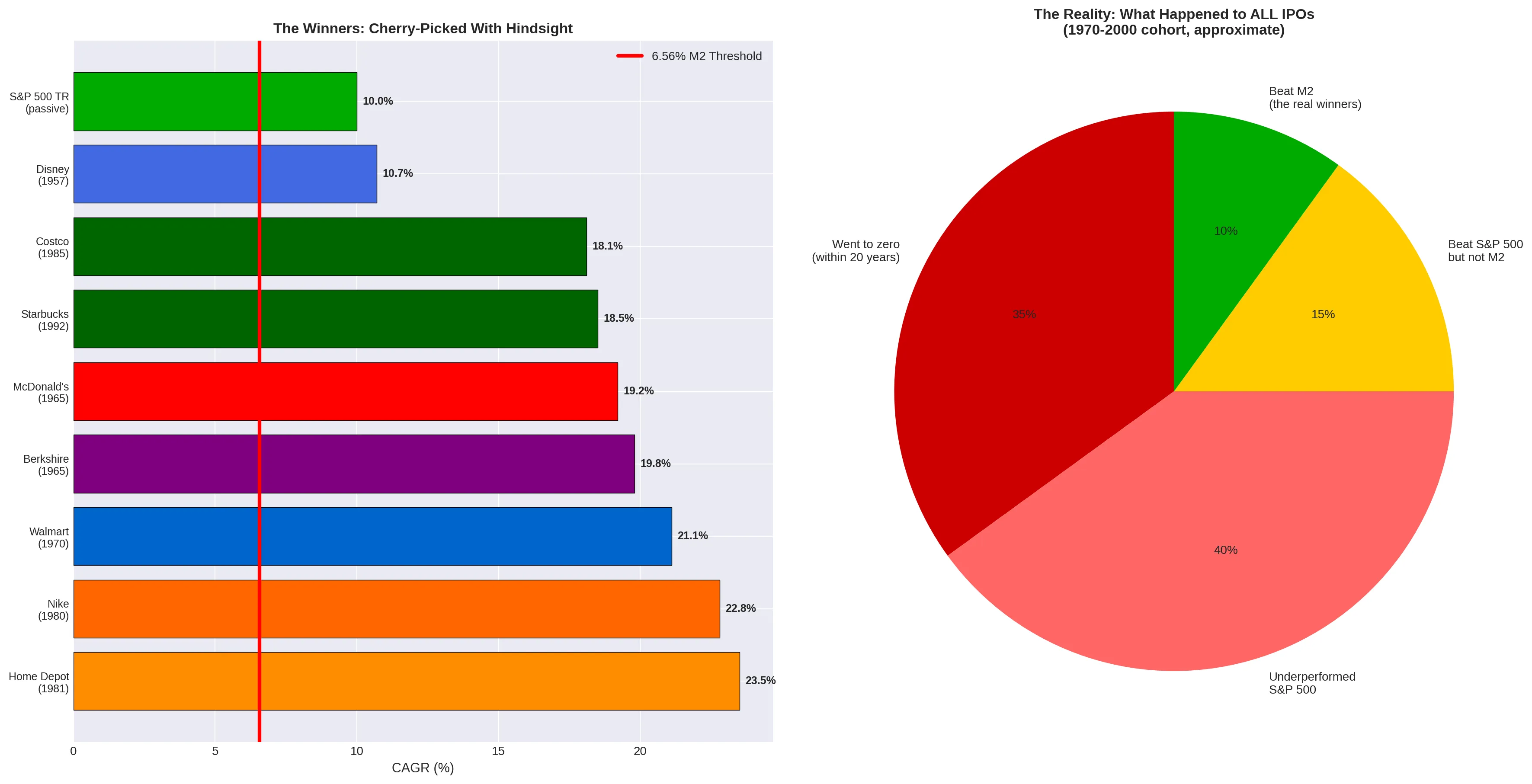

Looking at the table above, it is tempting to conclude that the path to wealth is simply buying good companies at their IPOs. However, this is a classic example of survivorship bias.

We are looking at the handful of companies that survived, thrived, and came to define global commerce. We are not looking at the thousands of retail chains, restaurant concepts, and apparel brands that went bankrupt during the same period.

Research into long-term IPO performance paints a grim picture for the stock-picker [4] [5]:

- Approximately 30–35% of IPOs go to zero or are delisted within 10 to 20 years.

- Another 40% underperform the S&P 500 over the long term.

- Only about 10–15% manage to beat the S&P 500 and outpace the expansion of the money supply (the 6.56% threshold).

To win the IPO game, an investor had to find the needle in the haystack, hold it through multiple recessions and market crashes (as explored in Part II), and resist the urge to sell after the stock had doubled or tripled.

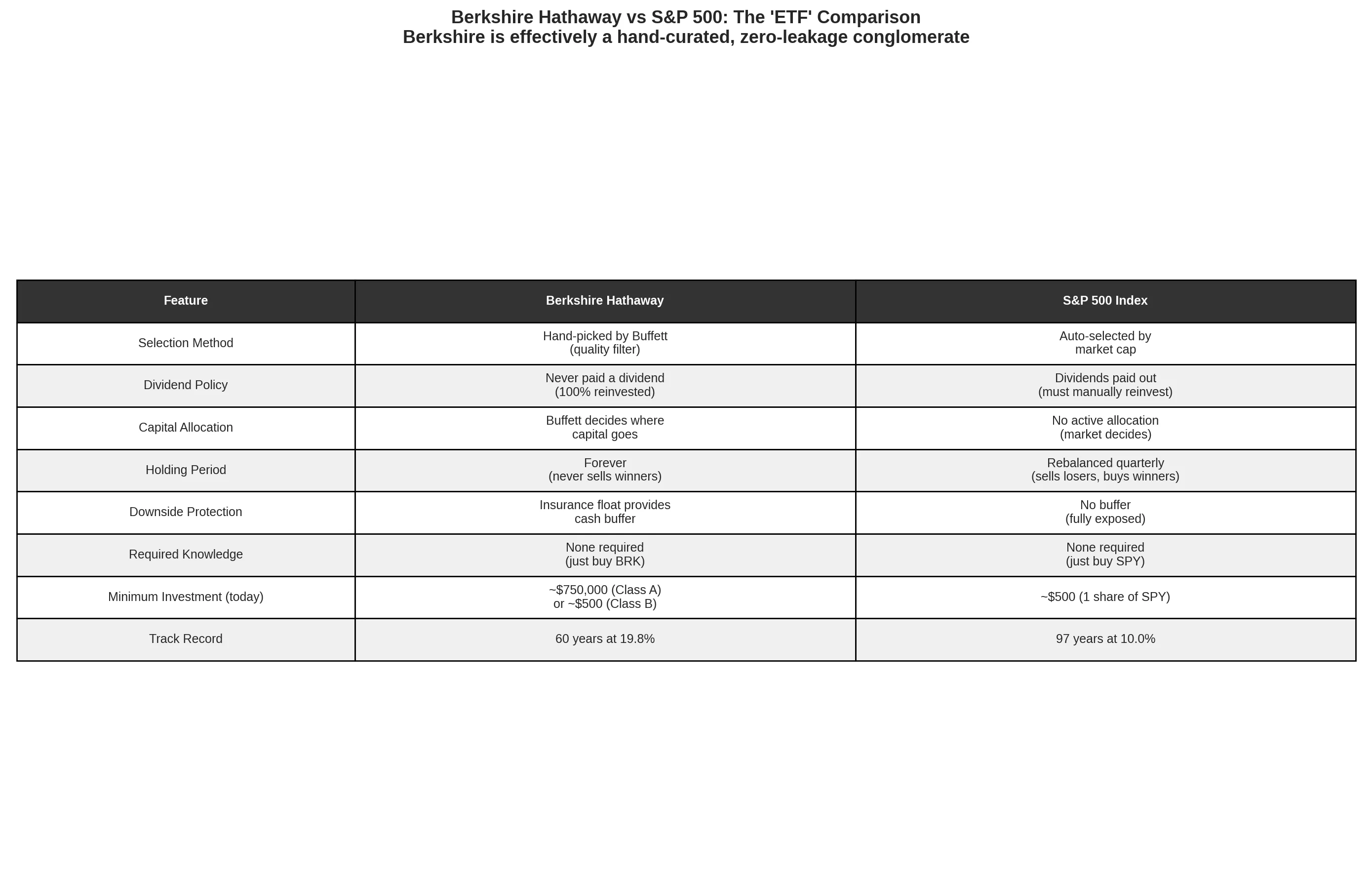

The Berkshire Advantage: The Ultimate “ETF”

This brings us back to the central question: If picking individual IPO winners requires perfect hindsight, what was the practical alternative?

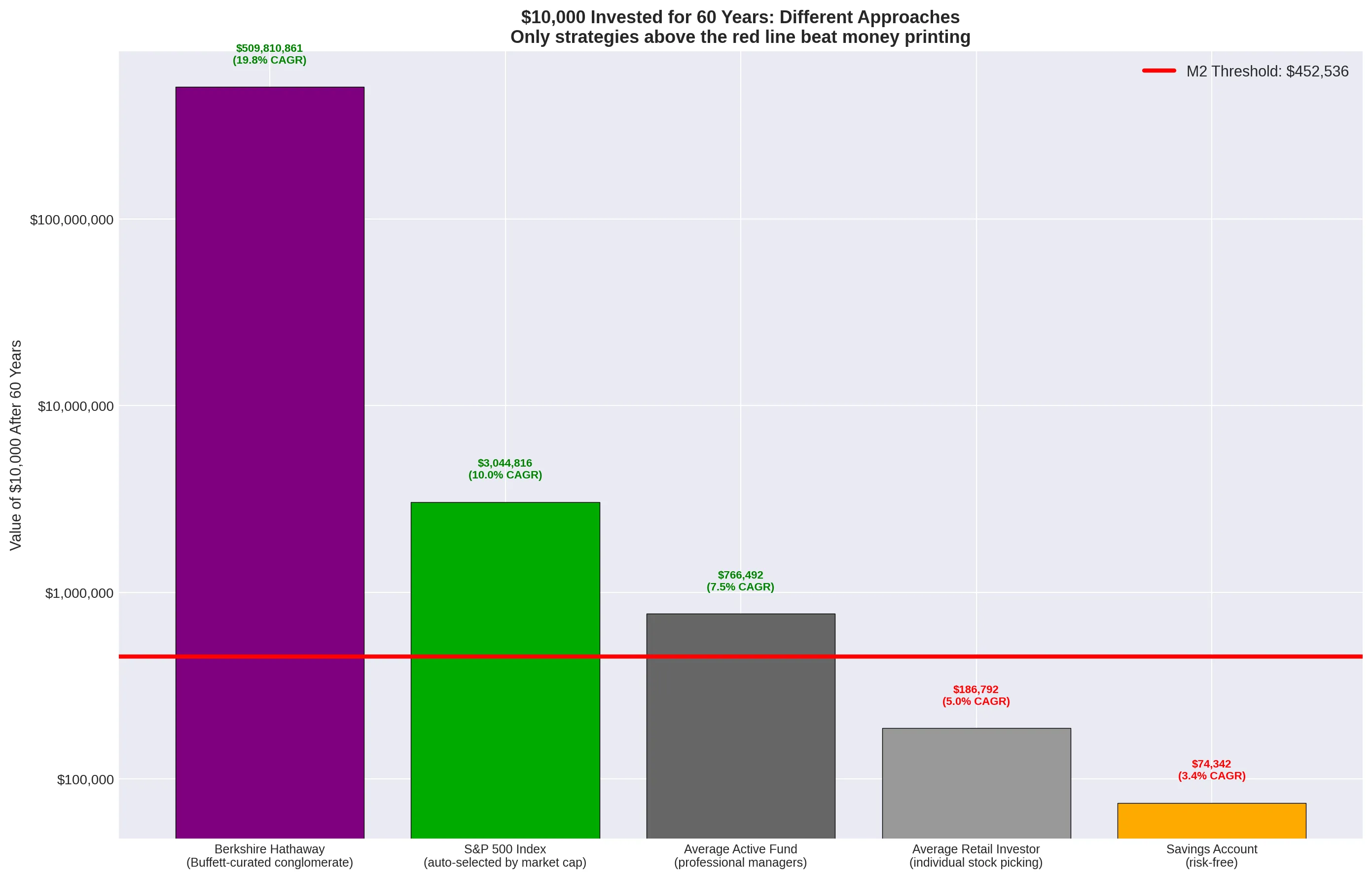

The S&P 500 Total Return was one answer, passively turning $10,000 into roughly $3 million over 60 years, and safely clearing the M2 threshold [6].

But Berkshire Hathaway offered something entirely unique. It was not a single operating business like McDonald’s or Home Depot, subject to the changing tastes of consumers or the disruption of its specific industry.

Instead, Berkshire was effectively a hand-curated ETF (Exchange Traded Fund) managed by arguably the greatest capital allocator in history.

- It required no stock-picking skill from the retail investor.

- It suffered from zero dividend leakage, as Buffett reinvested 100% of the profits tax-free within the corporate structure.

- It used insurance float to provide downside protection and leverage.

The chart above illustrates the massive divergence in outcomes based on the approach taken. The average retail investor, attempting to pick stocks without the benefit of hindsight, historically achieved around a 5% CAGR [7], meaning they actually lost purchasing power to the 6.56% monetary expansion rate.

Berkshire Hathaway was the anomaly: a single ticker symbol that provided the extreme outperformance of a successful IPO pick, but with the diversified safety of an index fund.

Conclusion: The Setup for the Digital Age

For the majority of the 20th century, the rules of the game were clear. To beat the printing press, you had to either:

A) Accept the passive 10% CAGR of the S&P 500 and wait 60 years. B) Possess the extreme luck required to pick the next Walmart at its IPO. C) Outsource your capital allocation to Warren Buffett.

In all three scenarios, the critical ingredient was time. It took 40 to 60 years for these compounding machines to achieve escape velocity from the expanding money supply.

But what happens when we look at the modern era?

In the last 30 years, the rate of money printing has accelerated dramatically. Have the traditional winners been able to keep up with this new pace? And more importantly, has the digital age (through the Nasdaq tech boom in Apple, Microsoft, Amazon, and Nvidia, or the invention of decentralised digital scarcity in Bitcoin) finally provided an asset class capable of outrunning the printing press in a fraction of the time?

Have the new digital assets achieved in 15 to 30 years what Berkshire and Walmart took 60 years to accomplish?

That is the question we will answer in Part V: The Digital Shift (1995–2025).

References

[1] Macrotrends LLC. “Historical Stock Price Data (MCD, WMT, NKE, COST, HD, SBUX).” [2] Yahoo Finance. “Historical Price Data and Splits.” [3] Federal Reserve Economic Data (FRED). “M2 Money Supply (M2SL).” Federal Reserve Bank of St. Louis. [4] Ritter, Jay R. “Initial Public Offerings: Updated Statistics.” University of Florida, 2026. [5] Gao, Xiaohui, Jay R. Ritter, and Zhongyan Zhu. “Where Have All the IPOs Gone?” Journal of Financial and Quantitative Analysis, 2013. [6] Damodaran, Aswath. “Historical Returns on Stocks, Bonds and Bills: 1928–2025.” NYU Stern School of Business. [7] Dalbar Inc. “Quantitative Analysis of Investor Behavior (QAIB) Report.”